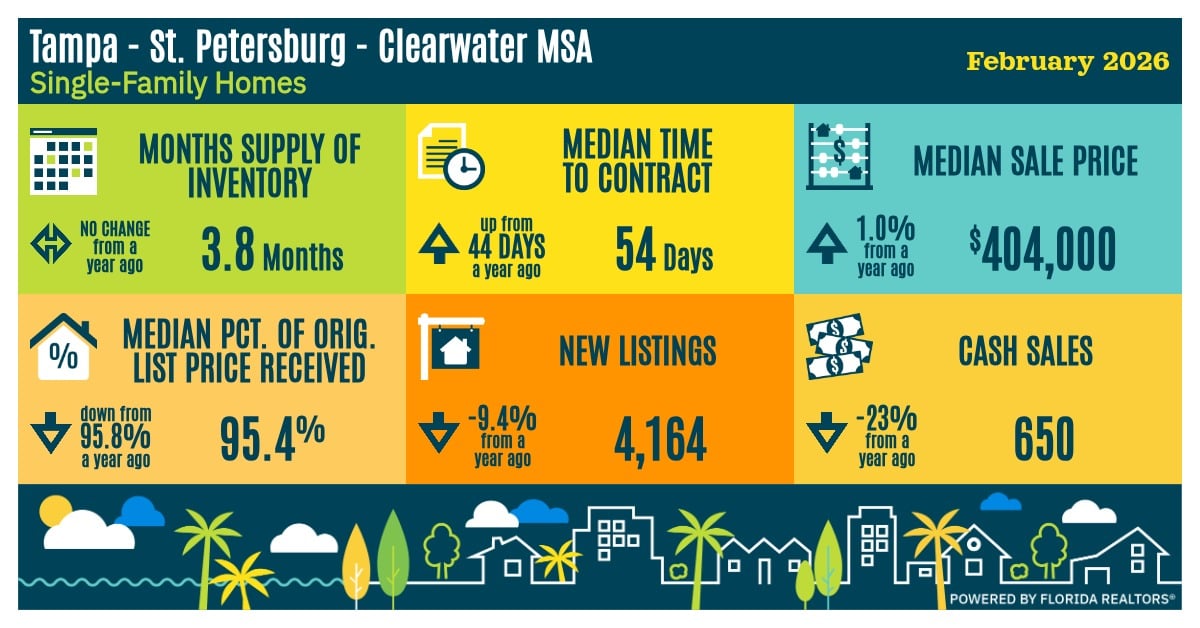

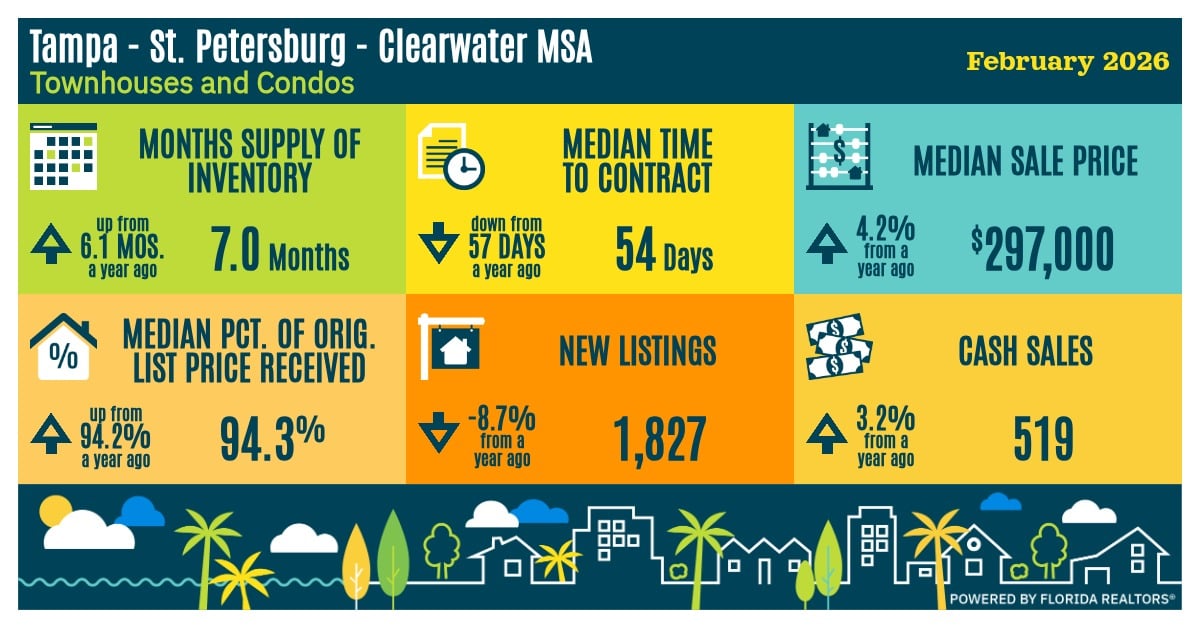

Florida’s housing market continued to show signs of stabilization and gradual improvement in February, according to the latest data from Florida Realtors. Closed sales increased for the sixth consecutive month, while pricing remained relatively steady across both major property types.

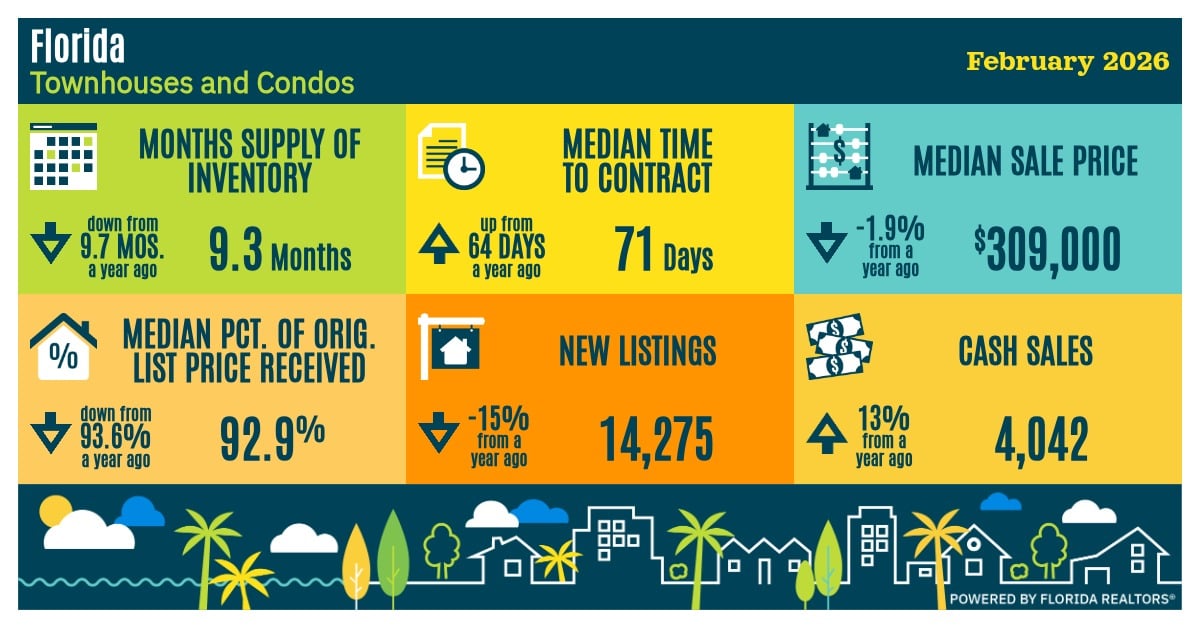

Single family home sales rose nearly 4% year over year in February, building on January’s strong performance. This marks six straight months of annual growth, with sales increasing in 16 of Florida’s 22 metro areas. Condo and townhouse sales also posted their sixth consecutive month of gains, climbing more than 8.5% year over year. While that increase outpaced single family homes at the statewide level, results were more mixed locally, with only half of metro areas seeing growth in this segment.

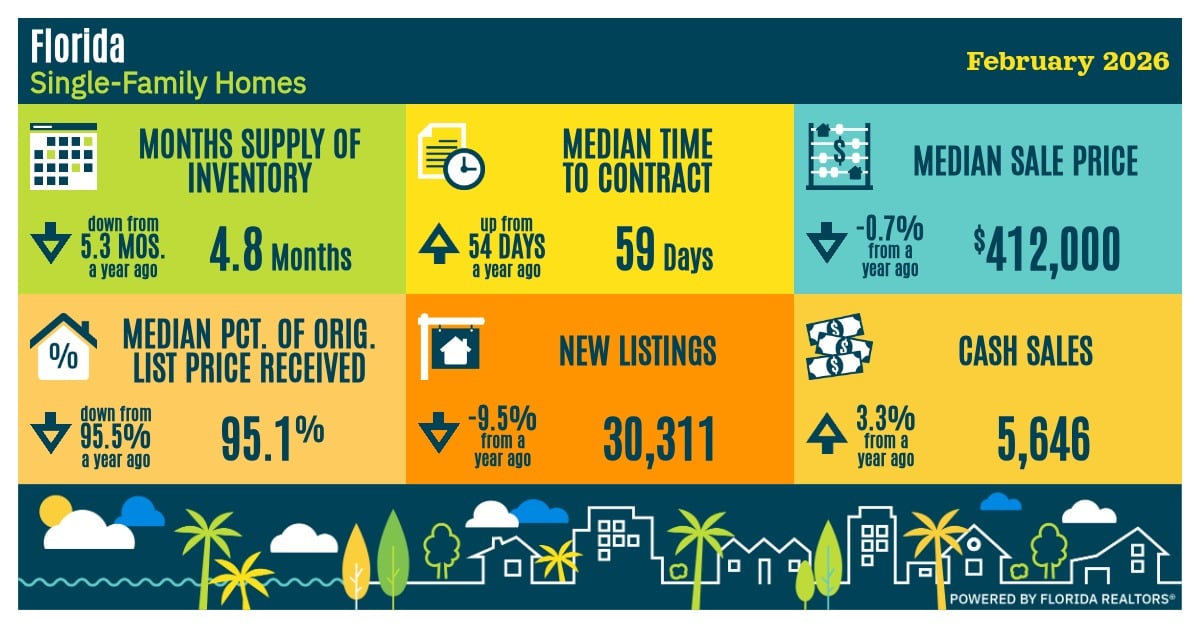

On the supply side, the surge in new listings seen at the start of the year eased in February. Single family new listings declined 9.5% year over year, while condo and townhouse listings fell more than 15%. Despite these declines, listing activity remains in line with pre-pandemic norms, suggesting a return to more typical seasonal patterns rather than a true pullback in supply.

Buyer activity also moderated slightly from January’s surge. New pending sales of single family homes were up about 4% year over year in February, down from stronger gains the prior month. Condo and townhouse pending sales rose just over 9%, also reflecting a more normalized pace of demand following an active start to the year.

One of the more notable shifts in February was on inventory. After a prolonged period of rising inventory since 2022, available listings declined year over year for the first time in several years. Single family inventory fell more than 7.5% compared to last year, with similar declines seen in the condo and townhouse segment. This tightening in supply is helping support current pricing trends.

Home prices remained relatively stable. The median sale price for single family homes was $412,000, down less than 1% year over year. Condo and townhouse prices came in at $309,000, down just under 2%.

Overall, February data suggests the Florida housing market has moved past its recent slowdown and is transitioning into a more balanced environment. Sales are trending upward, inventory growth has leveled off, and pricing remains steady. As always, local market conditions can vary, making it important to evaluate trends at the neighborhood level. If you’d like to explore what these trends mean for your real estate goals, whether you’re buying, selling, or just keeping an eye on the market, I'm always here to help!

Florida Data