Florida Statewide Market Overview | April 2024

Florida’s housing market continued to show signs of stability as the spring market moved further into full swing. April data reflected steady buyer activity, moderating inventory levels, and balanced pricing trends across much of the state. While month to month shifts can vary due to seasonal patterns, the broader year over year trends continue to paint an encouraging picture.

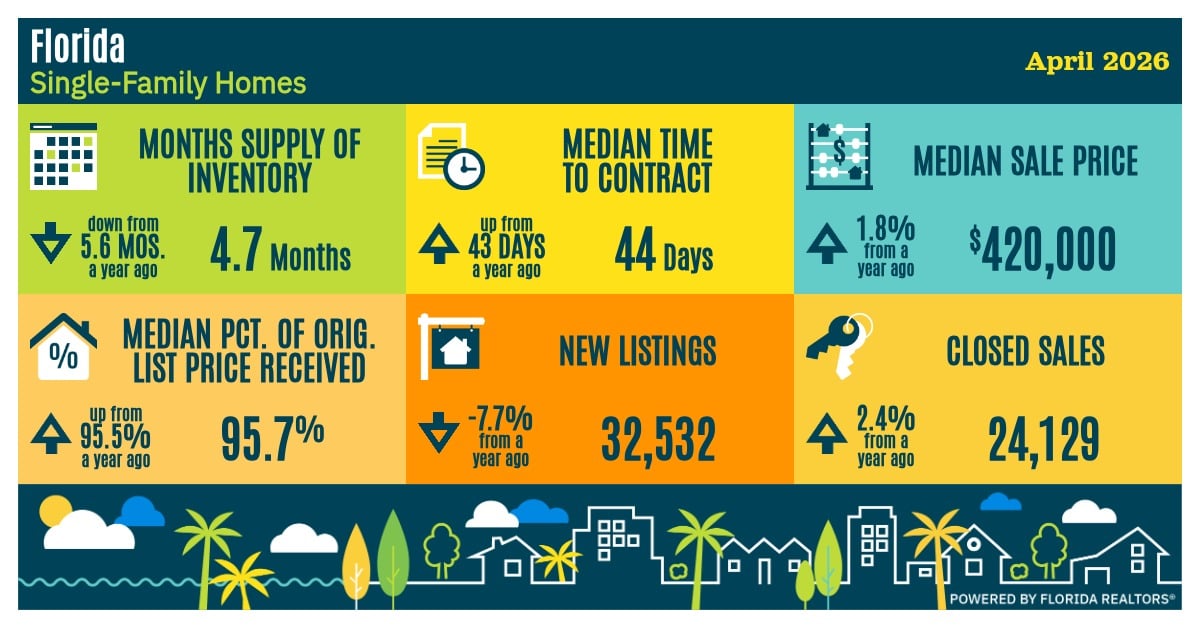

Closed sales of single family homes increased for the eighth consecutive month in April, rising nearly 2.5% year over year. Although this represented the smallest increase during the current growth streak, momentum remains positive. Looking ahead, pending sales data points toward continued activity, with new pending sales of single family homes jumping 8% year over year in April, more than doubling the pace seen over the prior two months. This suggests continued strength heading into late spring and early summer.

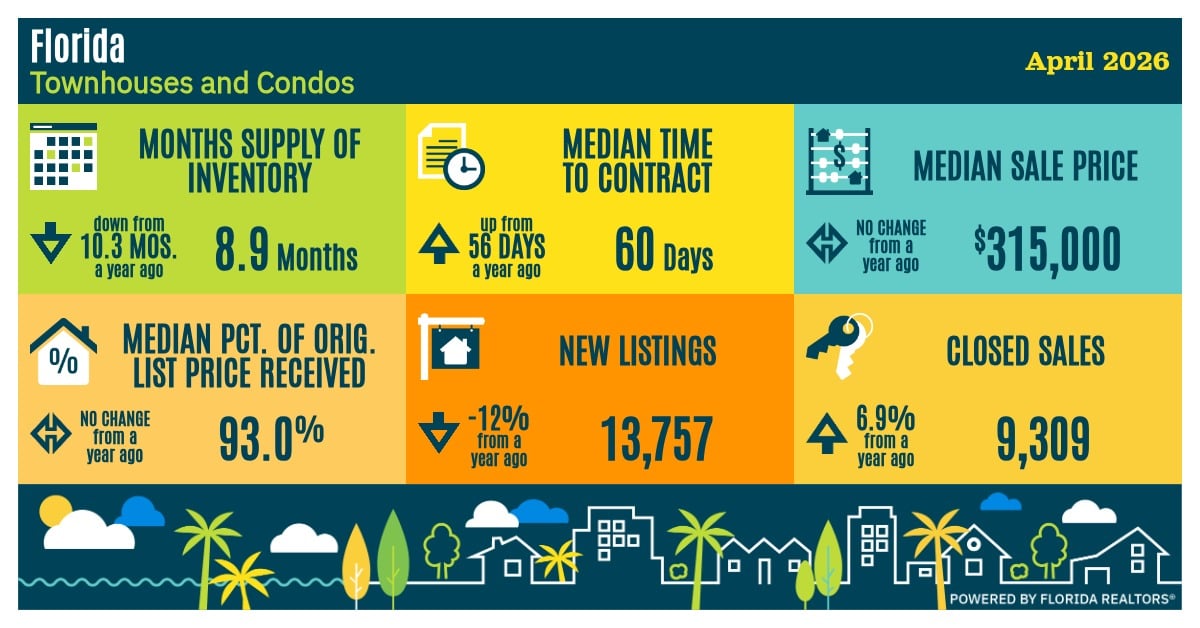

The condo and townhouse market also continued to improve. Closed sales increased approximately 7% year over year in April, outperforming single family homes for another month. New pending sales climbed nearly 15%, showing continued recovery after several years of adjustments tied to reserve requirements, financing challenges, and rising ownership costs. Affordability continues to make condos an attractive option for many Florida buyers.

On the supply side, new listing activity has begun settling into more normalized patterns. Single family new listings declined nearly 8% year over year in April, while condo and townhouse listings fell approximately 12%. However, these numbers are now tracking much closer to pre pandemic norms, suggesting a return to healthier and more traditional market conditions rather than signs of weakening inventory.

Inventory levels continued trending lower as improving demand and more measured listing activity worked together to tighten supply. Active single family inventory ended April nearly 14% below year ago levels, while condo and townhouse inventory declined 13.5%. Inventory levels statewide now appear much more in line with conditions seen from 2014 through 2020 rather than elevated levels associated with prior market corrections.

Homes are also moving at a more balanced pace. The median time to contract for single family homes was 44 days in April, only one day longer than a year ago and closely aligned with pre pandemic norms. Condo and townhouse properties took longer at 60 days, reflecting some of the additional complexity still present in that segment.

Pricing remained steady statewide. The median sale price for single family homes increased 1.8% year over year to $420,000, while condo and townhouse median prices held flat at $315,000. Overall, the Florida housing market continues to show signs of balance with steady sales activity, stabilizing inventory, and modest price movement as we head further into the heart of the spring market.

As always, local market conditions can vary, making it important to evaluate trends at the neighborhood level. If you’d like to explore what these trends mean for your real estate goals, whether you’re buying, selling, or just keeping an eye on the market, I'm always here to help!

Florida Data